incastle의 콩나물

Chapter7. The Capital Asset Pricing Model || Part.2 본문

Betas of Common Stocks

-

Beta value estimates are typically formed by using past stock values

베타 가치 추정치는 일반적으로 과거 주식 가치를 사용하여 형성됩니다. - Unless there are drastic changes in a company’s situation, its beta tends to be relatively stable

회사 상황에 급격한 변화가 없다면 베타는 상대적으로 안정적인 경향이 있습니다 - generally, aggressive companies or highly leveraged companies have high betas, whereas conservative companies whose performance is unrelated to the general market behavior are expected to have low betas

일반적으로 aggressive회사나 highly leveraged 회사는 베타가 높은 반면, 일반 시장 행동과 관련이 없는 보수적인 회사는 베타가 낮을 것으로 예상됩니다 - Companies in the same business are expected to have similar betas (but not identical)

Betas of a Portfolio

- Overall beta of a portfolio can be calculated using the betas of individual assets in the portfolio

- The portfolio beta is the weighted average of the betas of the individual assets in the portfolio, with the weights being the portfolio allocations

7.4 The Security Market Line

Security Market Line

-

CAPM formula can be expressed in graphical form by regarding the formula as a linear relationship

- This relationship is termed the security market line (SML)

- Under the equilibrium conditions assumed by CAPM, any asset should fall on the SML

모든 자산은 SML에 속해야합니다 - SML expresses the risk-reward structure of assets according to the CAPM

SML은 CAPM에 따라 자산의 위험 보상 구조를 표현합니다 - Emphasizes that the risk of an asset is a function of its covariance with the market, or equivalently, a function of its beta

- 자산의 위험은 시장과의 공분산의 함수 또는 이와 동등한 베타의 함수임을 강조합니다.

- 베타가 1일 때 수익률이 m이다!

Systematic Risk(체계적 위험)

-

CAPM implies a special structural property for the returns of an asset

-

This property provides further insight as to why beta is the most important measure of risk

-

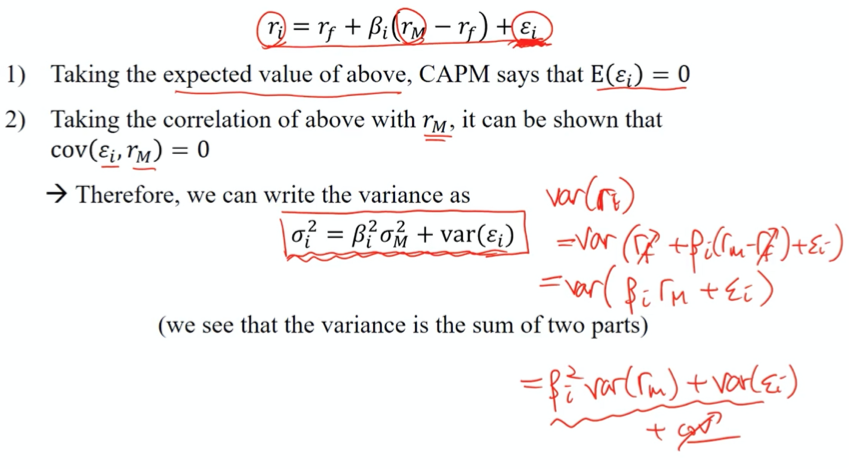

Let’s write the (random) rate of return of asset i as

-

CAPM formula tells us several things about 입실론_i(error term)

1) CAPM 공식이 만들어지려면 에러term이 0이어야 한다.

2) 에러term과 마켓 수익률 사이의 공분산은 0이다.

따라서 i의 분산은 두 개의 항의 합으로 이루어질 수 있다. 각각의 항에 대해서 자세히 살펴보면

- 분산 = risk이다. market과 관련된 risk는 asset i와 상관없이 존재하는 거니까, 분산투자해도 사라질 수 없음(체계적 위험) 하지만 비체계적 위험을 줄일 수 있음

7.6 Performance Evaluation

Performance Evaluation

- CAPM theory can be used to evaluate the performance of an investment portfolio

- It is indeed common practice to evaluate many institutional portfolios using the CAPM framework

CAPM 프레임 워크를 사용하여 많은 기관 포트폴리오를 평가하는 것이 실제로 일반적입니다.

CAPM의 이론에 비해서 실제 수익률이 높았는지 낮았는지 평가하기 => J라는 평가지표가 추가됨(알파라고도 함)

j가 0이라면 과거 10년 데이터를 넣었더니, capm수준으로 기대 수익률이 나온거고, j가 양수면 capm보다 더 높은 평균 수익률, 낮으면 낮은 평균 수익률을 의미한다.

7.7 CAPM as a Pricing Theory

Pricing Form of CAPM

-

CAPM is a pricing model

-

However, the standard CAPM formula does not contain prices explicitly

-

Suppose that an asset is purchased at price P and later sold at price Q

- capm은 주로 기대 수익률을 모델링하거나, 성과분석(알파 또는 베타) 할 때 주로 사용됨

- 물론 price를 표현하는 것도 가능은 하다.

(단순이 1/(1+이자율))로 하는 게 아니다 (random case이기 때문에)

'20-1 대학 수업 > 금융공학' 카테고리의 다른 글

| Chapter 8. Investment Science || Part.2 (0) | 2020.06.07 |

|---|---|

| Chapter 8. Investment Science || Part.1 (0) | 2020.06.05 |

| Chapter7. The Capital Asset Pricing Model (0) | 2020.05.17 |

| Chapter 6. Mean-Variance Portfolio Theory || Part 4 (0) | 2020.05.17 |

| Chapter 6. Mean-Variance Portfolio Theory || Part 3 (0) | 2020.05.17 |